Tax breaks continue to be the preferred option for financial advisers in Australia for correcting the country’s under-insurance issue according to a poll being run by RiskinfoNZ’s sister publication across the Ditch.

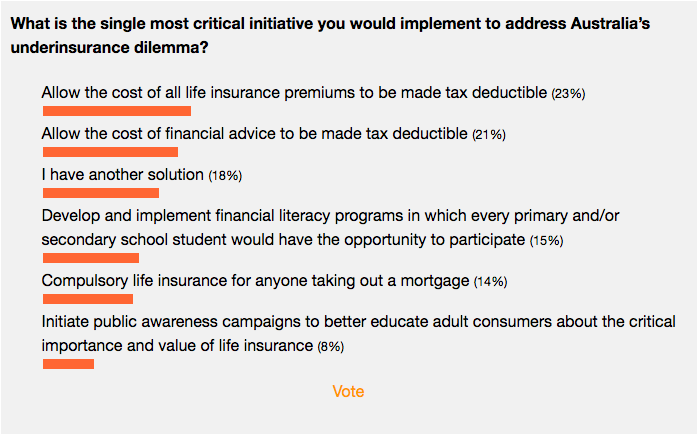

As we go to press, 23% of those voting in the Riskinfo Australia poll support the cost of financial advice being tax deductible. Meanwhile, 21% would prefer the cost of life insurance premiums to be tax deductible.

Unlike New Zealand, where a similar poll shows that 39% of voters agree the under-insurance issue is because of low levels of financial literacy, in Australia just 15% indicate this is an issue of concern.

Long-time contributor to Riskinfo, Jeremy Wright, may represent a number of his Australian peers when he makes this observation about the potential (unintended) damage being inflicted on the risk advice sector by regulatory reforms:

Separation of insurance and investment advice, an overhaul of the LIF and FASEA to encourage existing advisers to remain in the industry and provide an incentive to recruit risk advisers is the solution.

What we currently have is the exact opposite situation, which reflects the growing Under-insurance epidemic.

Below – the latest voting trend in Australia.

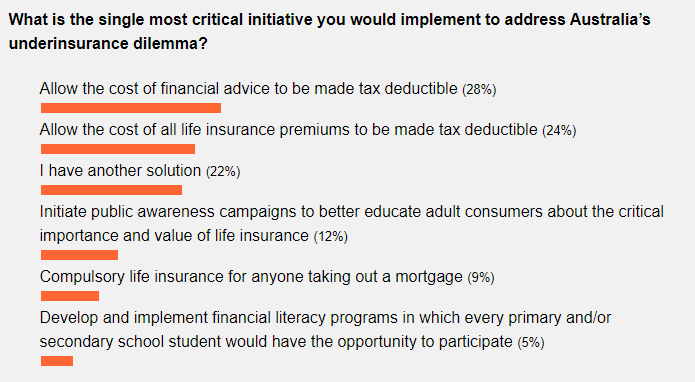

To date, the outcome of this latest poll closely reflects the result when the same questions were polled last year:

Ultimately, the resolution to Australia’s under-insurance dilemma will most likely be found in a combination of future actions.

In the current environment, however, there exist more pressing issues for many risk advice specialists, many of which revolve around the more immediate concern about the future viability of their business proposition.