News from the RBNZ that profitability in the life insurance sector has improved from previously subdued levels, and that the health insurance sector is under strain, attracted strong reader interest this week…

Profitability in the life insurance sector has improved from previously subdued levels, according to the RBNZ’s latest Financial Stability Report. However, it says the health insurance sector has come under strain over the past two years.

The bank’s November 2025 report, in a chapter entitled Institutional Resilience, says that in the life insurance sector, returns on equity remain low compared with other sectors and with alternative uses of capital “…maintaining pressure for further pricing or product adjustments.”

It says that while solvency margins in the life sector remain well above regulatory requirements, they have trended lower in recent years.

“This reflects a mix of insurers’ capital-management decisions, such as larger dividend payouts and re-calibrated target buffers, and technical changes in how solvency capital is measured, particularly for long-dated contracts.”

The bank says these factors have “…lowered reported margins, though overall capital positions remain Adequate.”

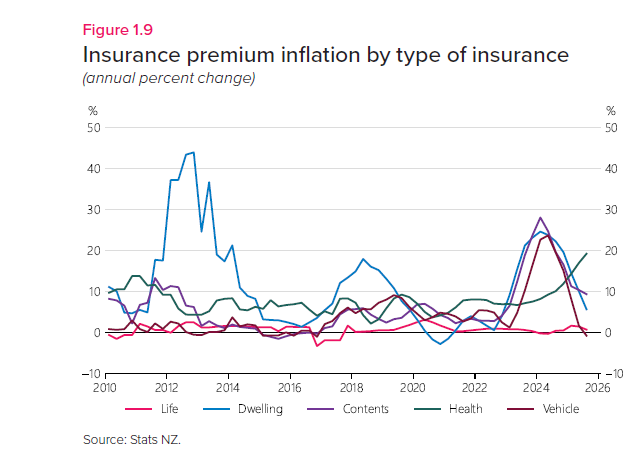

In more detail the report notes the health insurance sector has come under strain over the past two years, with sustained operating losses reducing solvency margins by nearly 40%.

“Insurers’ capital levels remain well above regulatory minimums. However, ongoing cost pressures mean premium increases will be needed to restore profitability so that the sector can sustainably provide services to policyholders and support the wider health system.”

…escalating claims costs have been the dominant source of strain in the sector…

It says escalating claims costs have been the dominant source of strain in the sector.

“From 2020 to 2022, medical cost inflation was within a typical range, accompanied by broadly proportionate premium increases. In recent years, capacity pressures in the public health system have resulted in more people turning to the private system.

“This increased utilisation of private health care has added to claims cost inflation. These domestic pressures are reinforced by global cost drivers, including the adoption of high-cost technologies, supply-chain disruptions, and rising labour costs.”

It says by 2023, many health insurers were reporting quarterly losses.

“Claims cost escalation intensified during 2024. The persistence of these pressures required insurers to reprice substantially,” the report states.

“From the second half of 2024, materially larger premium increases were implemented across the industry, both to recover earlier shortfalls and to restore profitability on a forward-looking basis.”

The bank says this contributed to strong growth in insurance revenue, with each of the past four quarters roughly 15 percent higher than the same quarter a year earlier.

“Despite this, the health insurance sector has continued to make losses to date. This reflects the lag between premium increases and the corresponding uplift in revenue, as policies are repriced gradually.”

…health insurers are repricing premiums, redesigning products, and implementing cost-management strategies…

Looking at sector and policy responses, the Reserve Bank says that in response to recent claims cost escalation, health insurers are repricing premiums, redesigning products, and implementing cost-management strategies.

“These measures intend to ensure products remain affordable and available in a high-inflation environment, but can result in narrower benefits or higher cost-sharing for customers.”

The bank says it has intensified its supervision of the sector and “…is closely monitoring solvency trends. Health insurers are now being included in the Reserve Bank’s stress-testing programme to assess resilience under scenarios of continued escalation of these pressures.”

It is also engaging directly with health insurers “…to ensure that responses support both the long-term sustainability of the sector and the resilience of households and the broader financial system.” Click here to see the full report.