Noted Australian actuary, John Trowbridge, is calling on his country’s Government, regulators and other industry stakeholders to reconsider the 60/20 risk commission model presently mandated under the Life Insurance Framework reforms.

Speaking at the 2020 FSC Life Insurance Summit during a panel session considering the current state of the Australian life insurance industry, Trowbridge said his main concern related to what he characterised as a crisis in the distribution of retail life insurance.

He noted the significant reduction in the number of life insurance advisers in recent years, meaning less Australians, especially those in the middle market or mums and dads sector, are receiving access to critical life insurance advice.

Role of Advisers

In proposing a revised remuneration structure for risk advice, Trowbridge emphasised that, while some industries may be able to rely on direct access and commoditised products, when it comes to life insurance advice, that model doesn’t work. He maintains that for life insurance to be accessed properly by consumers it needs to be accompanied by advice.

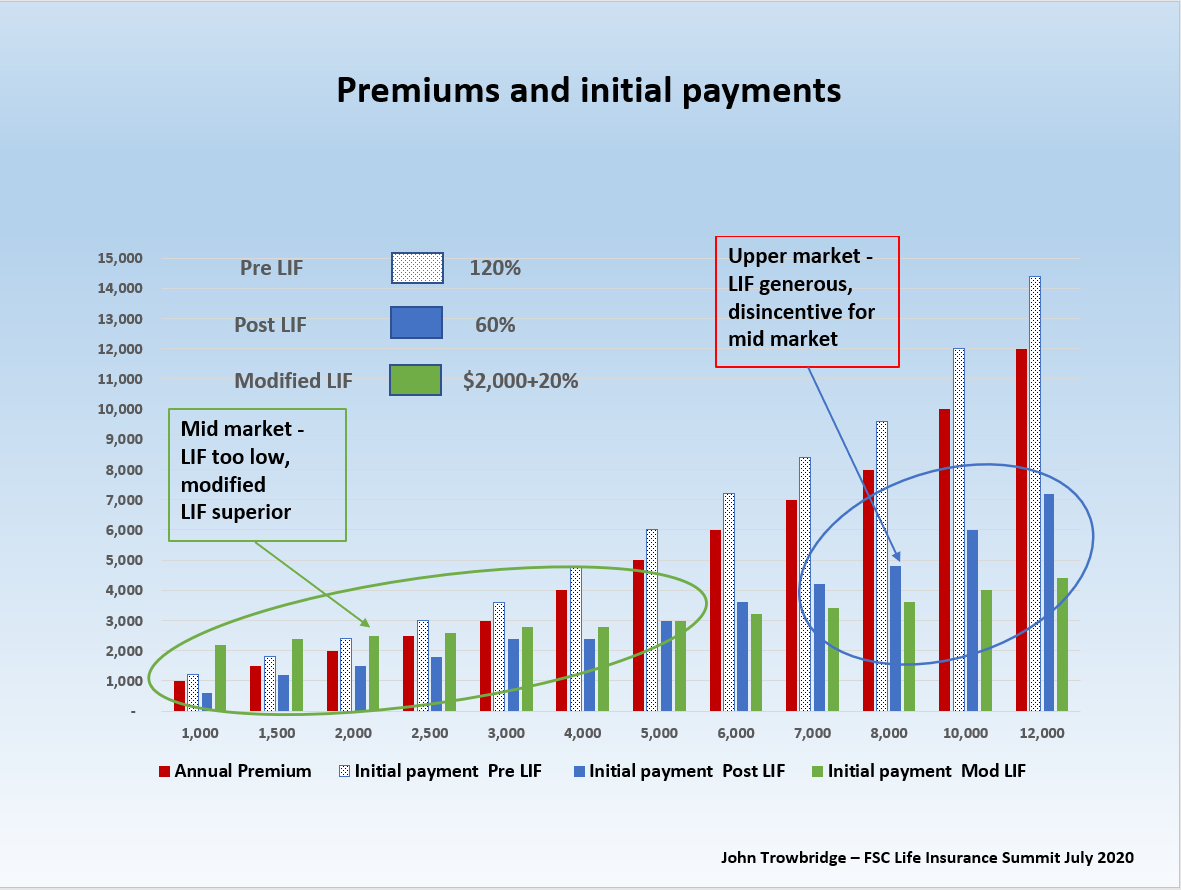

…the implementation of the 60/20 commission model …has limited the ability of advisers to deal with their customers

Trowbridge acknowledged and supported the agenda of both Government and regulator to serve the best interests of the consumer by the removal of misaligned incentives and conflicts of interest. However, he warned that the implementation of the 60/20 commission model under the LIF reforms, when combined with stringent SoA and other regulatory requirements “…has limited the ability of advisers to deal with their customers.”

In order for risk advisers to have the commercial capacity to provide advice to the mums and dads market, Trowbridge proposes a revised model which effectively reduces remuneration levels on higher sums insured but makes it more attractive for advisers to deal in the mid-market:

The structure of Trowbridge’s recommendation mirrors the remuneration model for life insurance advice he initially proposed in 2015 in the final version of what has become known as the Trowbridge Report, namely the report from the independent chair (Trowbridge) of the Life Insurance and Advice Working Group (see: 20% Flat Commissions – Trowbridge).

Rather than the $1,200 Initial Advice Payment (IAP) proposed by Trowbridge in 2015, his revised model in 2020 advocates for a $2,000 IAP to be paid to advisers, accompanied by a flat 20% commission annual payment.

According to Trowbridge, either at the FSC Life Insurance Summit session or in speaking later with Riskinfo, his revised proposal delivers the following benefits:

- Assuming an average cost of $2,000 – $3,000 to place a life policy on the books, the new model gives advisers the commercial ability to deliver life insurance advice to the mums and dads market

- Removes any clawbacks of upfront commissions because only renewal commissions are payable in conjunction with the $2,000 IAP

- Observes the Government and regulator’s agenda to better align the interests of advisers and their clients while removing or significantly minimising any conflict of interest, real or perceived

This new model does not remunerate the adviser if no life insurance policies are placed as a result of the advice. However, this has always been the case, whether it applies to the LIF remuneration model or to the open commission system it replaced.

Trowbridge told Riskinfo he appreciates the remuneration recommendations contained in his final report in 2015 generated significant opposition from advisers and adviser associations, particularly the AFA, which was a participant on the Life Insurance and Advice Working Group, but which did not support his final recommendations.

With a view to finding a solution, however – which would enable risk advisers to financially survive and prosper while serving the life insurance needs of middle Australia – Trowbridge said advancements will have been made if the debate becomes about the numbers he proposes (i.e. the level of the IAP and renewal commission), rather than the structure of the underlying model itself.

Editor’s Note: We welcome your considered and measured comments on this article, as part of an ongoing debate which attaches to the future viability of life insurance advice in Australia.