An Actuaries Institute Taskforce in Australia has made sweeping recommendations for broad changes to the country’s retail disability income insurance market “…to reset sustainability for a sector under threat”.

Taskforce Convenor Ian Laughlin says, in a statement, that without an overhaul those who need cover may not be able to afford it in the future and life insurance companies selling individual disability income insurance policies will continue to suffer large losses.

He says this is neither in the interests of customers nor the community at large.

Laughlin says the sector must offer products that provide more certain outcomes, are more easily understood by consumers with features and prices that better meet their needs.

The statement says that the taskforce recommendations, which are being circulated widely for stakeholders’ consideration, include a review of the law around life insurance, so insurers can better take into account fundamental changes to the way society views disability and returning to work.

It issues a warning that regulators will continue to intervene until the sector shows sustainable improvements in practices and outcomes.

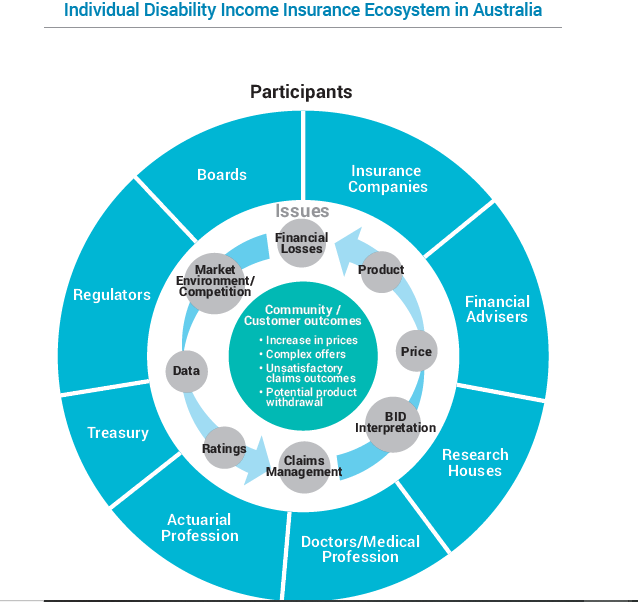

It adds that individual disability income insurance policies provide critical cover for those who may lose their income because of disability. About 850,000 policies are currently on issue, which is an indicator of the importance of the market, it says. But the taskforce formed the view that “…the market is at risk of failure”.

Hoa Bui, President of the Actuaries Institute and a key member of the taskforce says in the statement that the lack of sustainability of the disability insurance market is one of the most pressing issues for life insurers today.

“We’ve looked at the issues through a consumer lens to find a way forward for all parties,” she says.

The report Disability Insurance Income Provisional Findings and Recommendations states “the product has become more and more complex over time, making it difficult for customers to understand and be satisfied with claims outcomes. At the same time, affordability and accessibility for those needing cover is declining.

“Increasingly, those with cover are finding the cost prohibitive, and the more-healthy policyholders are then likely to not maintain cover.”

…Increasingly, those with cover are finding the cost prohibitive, and the more-healthy policyholders are then likely to not maintain cover…

The report, which includes findings, recommendations, and a paper on the framework for a ‘reference product’ for risk and uncertainty assessment, involved input from more than 40 actuaries, and discussions with regulators ASIC and APRA, Treasury, CEOs, boards, lawyers, consumer advocates, claims and underwriting professionals, doctors and financial advisers.

It follows the release earlier this year of a KPMG research paper, commissioned by the institute, that found life companies lost $3.4 billion over five years by selling complex products to individuals which, ultimately, threaten the viability of the sector (see: New Call for Reform of Disability Insurance Sector).

The statement adds that the taskforce has not taken into account the likely negative impact of Covid-19 on future claims.

Outcomes the taskforce hopes to achieve after further industry input include:

- Product features, underwriting and claims practices that promote closer alignment between consumers and providers of insurance

- Stable prices over time

- Sustainable outcomes for insurers

- Community confidence around fairness and the enduring value of the insurance

The statement from the institute says that a failure to bring about reform would result in loss of productivity in communities, a rise in demand for community and family-based support, increased social security costs and, for those who need support, a decline in mental health, a loss of confidence and self-worth.

Recommendations include:

- Insurers gain better insights into customer claims experience

- Simpler and cheaper products with a focus on return to health and work

- Strong controls over the level of benefits paid

- Products that can be updated to allow for advances in medicine, technology and society’s expectations

- Sustainability heat maps and a review of board composition to ensure risks are understood and managed

- Clear examples of best interest duty and changes to product ratings

- Standardised collection of medical information and better underwriting and claims data

“The taskforce strongly believes that the problems are more deep-seated and diverse” than just product terms and conditions, Laughlin says, adding that CEOs believe the product has lost the principle of indemnity, and had said there was too much capital invested in a market with a relatively small base. Boards may not receive the right analysis to allow directors to understand the extent of long-term guarantees and risks.

Laughlin says that loss minimisation, a feature of many other insurance contracts, is not explicitly expressed in disability income insurance contracts. Should those making claims have a duty to return to work as soon as possible to minimise benefits paid to them, especially where a return can aid recovery?

He adds the rise in mental health claims and community expectations around return to work rates are not easily accommodated, and Treasury and APRA should review the 1995 Life Insurance Act to test whether it remains fit for purpose.

The next steps include stakeholder and industry feedback. Consultations close on October 31.

Click here to see the full report.