While RiskinfoNZ’s latest poll result finds a majority of New Zealand financial advisers don’t agree with the FMA focus on monitoring the advice sector regarding conflicts arising from risk commission structures, Australian advisers seem very keen indeed that their Government review the commission caps that prevail in their life insurance market.

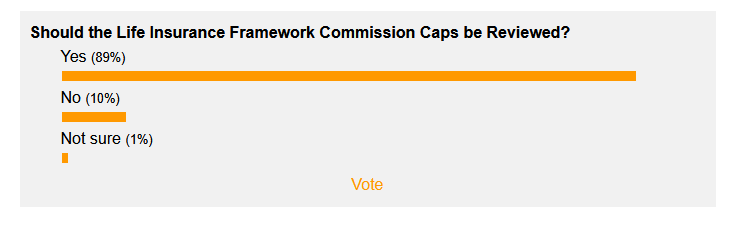

Our Australian sister publication canvassed advisers on whether the Australian Life Insurance Framework 60/20 commission caps should be reviewed, with an unsurprising 89% of advisers indicating they should be – with just 10% disagreeing (see: United Voice – Review Risk Commissions).

While the FMA is just beginning its monitoring to ensure FAPs here have effective processes and controls in place to manage conflicts of interest arising from commissions, the Australian financial advice sector has been grappling with the fallout from ASIC’s Review of Retail Life Insurance Advice (ASIC Report 413) since October 2014.

This culminated in the capping of risk commissions under the Life Insurance Framework reforms to their current hybrid 60/20 levels.

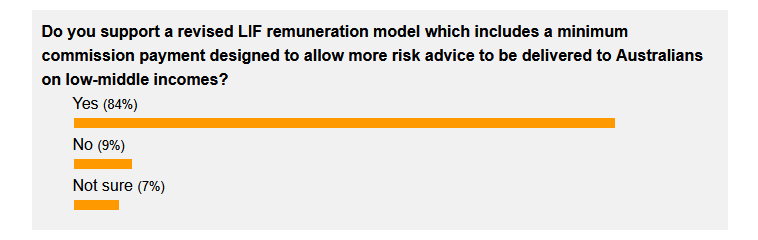

Twelve months earlier Riskinfo in Australia had asked its readers whether the LIF remuneration model should include a minimum commission payment designed to allow more low-middle income Australians to access risk advice, with the results seeing advisers sending a strong message in support of a proposition to restructure the LIF commission caps.

The latest message, it seems, from Australian advisers is that it’s time for the Australian Government to act on risk commissions as the life insurance industry there continues to suffer the consequences of fewer advisers, lower levels of new life insurance being written and fewer Australians accessing the life insurance advice needed by so many.